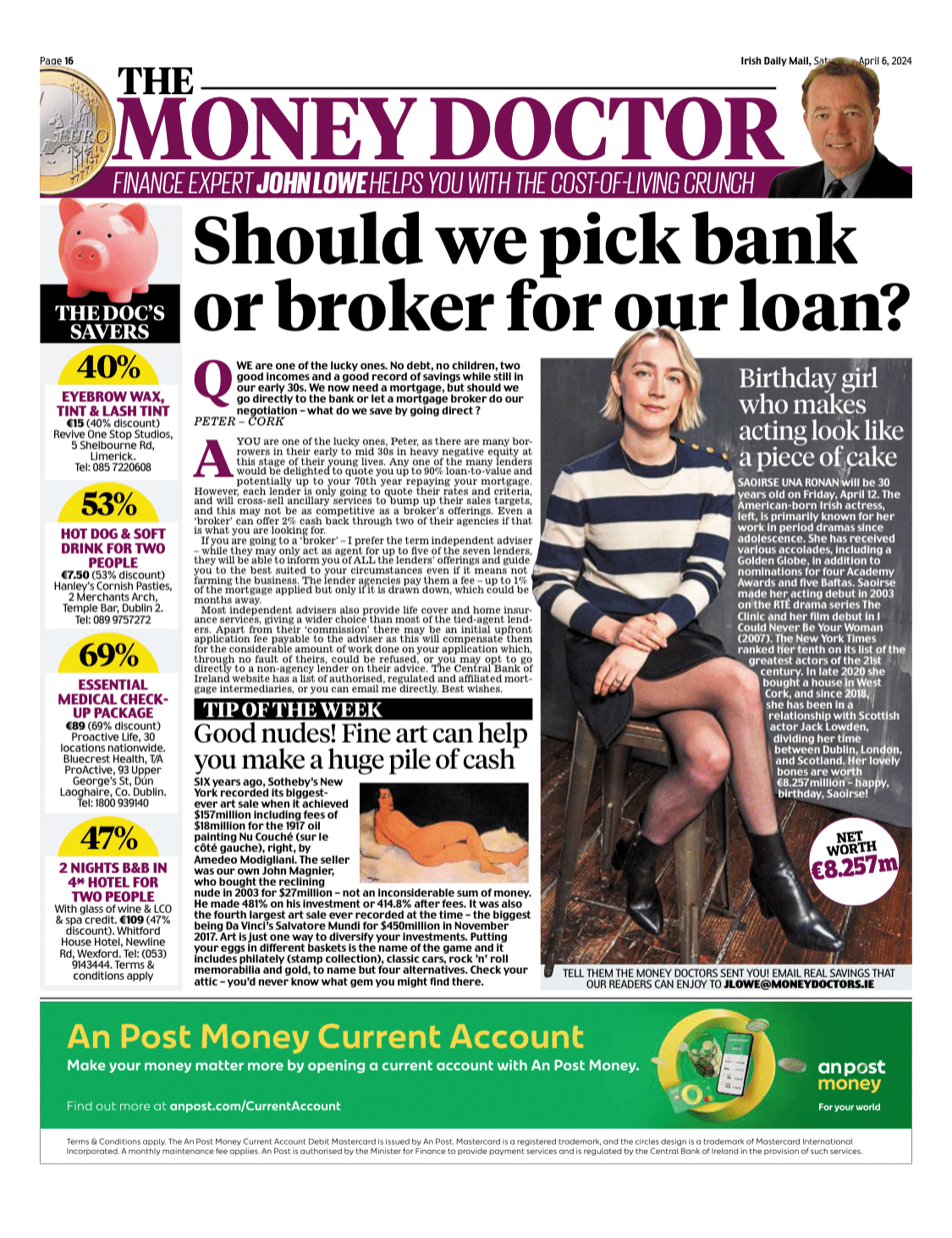

Q – We are one of the lucky ones. No debt, no children, two good incomes and a good record of savings while still in our early 30s. We now need a mortgage but should we go direct to the bank or let a mortgage broker do our negotiation – what do we save by going direct ? Peter – Cork

A – You are one of the lucky ones Peter as there are many borrowers in their early to mid 30s in heavy negative equity at this stage of their young lives. Any one of the many lenders would be delighted to quote you up to 90% loan to value and potentially up to your 70th year repaying your mortgage. However each lender is only going to quote their rates and criteria plus will cross-sell ancillary services to bump up their sales targets that may not be as competitive as a broker’s offerings. Even a “broker” can offer 2% cash back through two of their agencies if that is what you are looking for.

By going to a “broker” – prefer the term independent adviser – while they may only act as agent for up to five of the seven lenders, they will be able to inform you of ALL the lenders’ offerings and guide you to the best suited to your circumstances even if it means not farming the business. The lender agencies pay them a fee – up to 1% of the mortgage applied but only if it is drawn down, which could be months away.

Most independent advisers also provide life cover and home insurance services giving a far wider choice than most of the tied-agent lenders. Apart from their “commission” you can appreciate there may be an initial upfront application fee payable to the adviser as this will compensate them for the considerable amount of work done on your application which through no fault of theirs, could be refused or you decide to go directly to a non-agency lender on their advice. The Central Bank of Ireland website has a list of authorised, regulated and affiliated mortgage intermediaries or email me directly. Best wishes